Mortgage Rates Drop – Is Now the Time to Secure Your Best Deal?

After years of turbulence in the housing and mortgage market, we may finally be seeing the first real signs of stability returning. Recent news that two-year fixed mortgage rates have fallen below five-year rates for the first time since 2022 has caused a bit of a stir—not just among property industry professionals, but also among homeowners, first-time buyers and landlords. At Benwell Daykin Estate Agents, we don’t just sell and let properties—we also offer clear, tailored mortgage advice to help you make sense of the numbers and secure the best possible deal. With the latest rate changes, many people are asking the same question: Should I act now?

What’s Changed in the Mortgage Market?

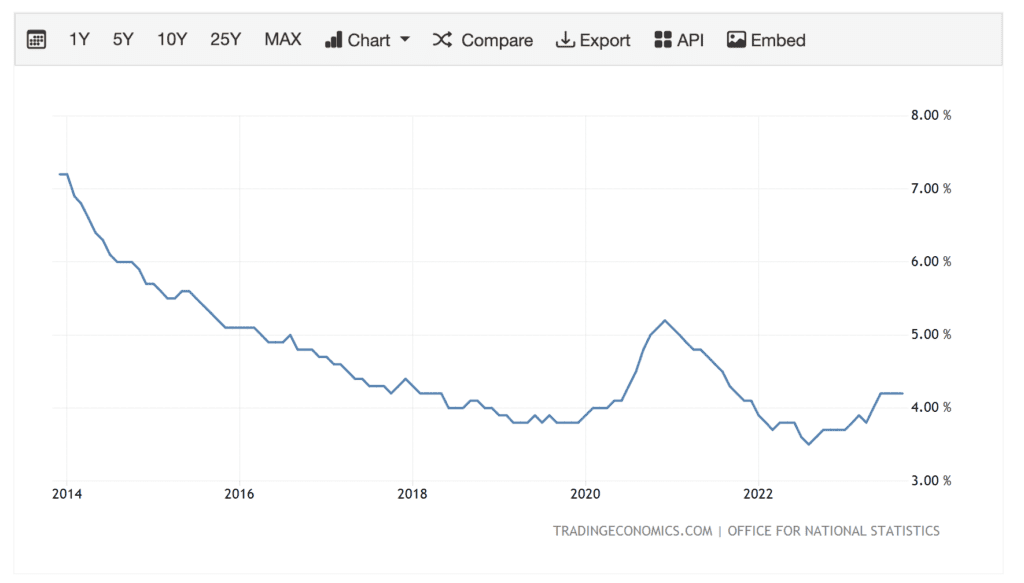

The Bank of England has made the decision to cut the base rate by 0.25 percentage points to 4%. This move was widely anticipated as inflationary pressures eased, but its impact on mortgage pricing has been swift. For the first time in nearly three years, two-year fixed rates have dipped below five-year deals. Historically, this has been the norm, but the upheaval following the 2022 mini-budget turned the market on its head, with lenders pricing shorter-term fixes higher due to uncertainty. Now, average two-year fixed rates sit around 5%, slightly lower than the 5.1% average for five-year terms. And for borrowers with a strong credit profile and good loan-to-value (LTV) ratio, some lenders are offering two-year rates as low as 3.8%. This shift suggests lenders are feeling more confident about the market’s direction—something we haven’t seen for a while.

Why This Matters for Homeowners and Buyers

For anyone on a variable or tracker mortgage, the benefits are immediate—monthly payments will likely fall in line with the base rate cut. But for those on fixed deals or looking to buy, the picture is a bit different. Here’s why the changes could be significant for you:

1. Opportunity for Lower Payments in the Short Term – A competitive two-year fix could mean lower monthly payments compared to sticking with your current deal or opting for a longer term at today’s rates.

2. Flexibility – If rates continue to drop in the coming years, being on a shorter fix allows you to refinance sooner and potentially secure an even better rate later.

3. Confidence Boost for Buyers – Lower rates can improve affordability calculations, meaning you might be able to borrow slightly more or widen your choice of properties.

A Word of Caution

While this is positive news, it’s important not to get caught up in “lowest rate fever” without looking at the bigger picture. Mortgage rates are only one part of the equation. You also need to consider arrangement fees, early repayment charges, flexibility to make overpayments, and whether your circumstances might change during the term. This is where speaking to a qualified mortgage adviser—someone who can look at your full financial situation—becomes invaluable. You can speak to someone today by calling 0115 990 2007.

The Benwell Daykin Approach to Mortgage Advice

At Benwell Daykin, we believe that mortgage advice should be personal, jargon-free and focused entirely on your best interests. Whether you’re a first-time buyer, remortgaging, or expanding your buy-to-let portfolio, we start by understanding you. Our free initial mortgage advice session is designed to: review your current deal and see if you could save money; explore the full range of mortgage products from across the market—not just one or two lenders; run affordability and repayment calculations tailored to your budget; highlight any hidden costs or restrictions in potential deals; and help you decide whether now’s the right time to fix, or if waiting could be wiser. We know that your mortgage is likely the biggest financial commitment you’ll ever make. That’s why our advisers take the time to guide you step-by-step, without pressuring you into a decision.

Why the Market Shift Feels Different This Time

Mortgage rates have had their ups and downs in recent years, but the fall we’re seeing now is being met with cautious optimism from industry experts. This is because it’s not just about cheaper borrowing—it’s about the return of market balance. For most of the past three years, the so-called “inverted curve” (where short-term rates were more expensive than longer ones) signalled lender uncertainty. Now, with two-year rates back below five-year deals, it reflects a belief that inflation will remain under control and the Bank of England won’t have to keep rates elevated for as long as feared. For homeowners, this could be the start of a more predictable, less volatile lending environment. And that’s good news whether you’re remortgaging this year or just starting to think about buying.

What This Means for First-Time Buyers

If you’re stepping onto the property ladder for the first time, these rate cuts could improve your affordability calculations, allowing you to borrow more or access a better deal. However, it’s important to remember that property prices, deposit requirements, and credit history still play a big role in what you can secure. That’s where our advisers can help you plan your move strategically—sometimes even months in advance—so when the right property comes up, you’re ready to act.

What This Means for Those Remortgaging

If your current deal ends within the next 6–12 months, now is the time to start exploring your options. Many lenders will allow you to lock in a new rate up to six months before your existing deal ends, which could protect you against future rate rises. Even if you’ve still got longer left on your fix, it’s worth checking whether an early switch could still save you money in the long run—especially if the rate difference is significant.

The Risk of Waiting Too Long

While rates have dropped, there’s no guarantee they will keep falling. Economic conditions, inflation data, and central bank policy can change quickly. If you’re in a position to secure a good rate now, it might be safer than holding out for something marginally better that may never materialise. Our role at Benwell Daykin is to help you weigh the potential benefits of acting now against the possible gains of waiting—backed by real market data and lender insights.

Why Choose Benwell Daykin for Mortgage Advice?

We work for you, not the banks – our recommendations are based solely on what’s right for your situation. Whole-of-market access – we can search deals from dozens of lenders, including smaller building societies and specialist providers. Clear, no-nonsense guidance – we explain the pros and cons in plain English. Free initial consultation – no cost, no obligation, just expert insight to help you make an informed choice. Local knowledge – based in Nottingham, we understand the property market in your area.

Next Steps – Take Control of Your Mortgage

If you’re a homeowner, first-time buyer, or landlord, this shift in rates could be your opportunity to get ahead of the curve. But the key is acting on accurate, personalised advice—not guesswork. Your mortgage shouldn’t keep you awake at night. Let us take the stress out of the process and help you find the deal that fits your life, not just your numbers.

Book your free initial mortgage advice session today with Benwell Daykin Estate Agents.

Call us on 0115 990 2007 or contact us here.