Benwell Daykin’s annual colouring competition is back!

Every year, Benwell Daykin Estate Agents runs a competition in line with Easter.

The competition has several different age categories, with a simple Easter design for children and a more complex design for adults.

Whether you have children who would like to take part, or if you simply want to put your adult colouring skills to the test, download our 2024 Easter designs here.

Please return entries to the office on High Street in Ruddington by 29th March 2024.

And if you’d like to find out how much your property is worth with a free valuation, we can speak to you about this at the same time!

Good luck to everyone taking part and Happy Easter!

Many people across the UK are asking when will mortgage rates will drop?

For those who already own a property, the prospect of remortgaging may seem daunting since rates increased in 2023.

Those looking to move to a new property may also be waiting for mortgage rates to drop to make their next purchase just that bit more affordable.

When will mortgage rates drop?

The good news is that they are starting to drop already.

It was reported this week that rates dropped below 4% at Nationwide, the UK’s largest building society. The rate is 3.84% at the time of writing.

This is the cheapest deal provided by the company for 8 months and is also significantly under the Bank of England’s base interest rate.

This is only available currently to those who are remortgaging although it’s still not bad news for first time buyers; the rate offered to those looking to take a first step onto the property ladder is only 0.01% higher at 3.85%.

Both these products are 5 year fixed rate deals and are significantly lower than the average offered by other lenders which stood at 5.2% this week.

Will other mortgage lenders follow suit?

Although some lenders are following the trend of sub 4% products, some are actually increasing.

Santander recently increased their rates on some mortgage products by 0.2% for remortgages.

This though is still well below the average last summer when rates stood at around 6%.

Should you wait for rates to drop further?

Unfortunately, we don’t have a crystal ball which will tell us the future relating to mortgage rates.

As we’ve seen this week, rates can go up and down and fluctuate daily.

For now, we feel that rates are likely to stick at around this mark for the next few months.

The best advice we can give at Benwell Daykin is always talk to our qualified mortgage broker who will be able to advise you in more detail.

Products can vary depending on your own circumstances too, so it’s always a good idea to compare the whole of the market with a broker and find out which products match your criteria.

For some, this will now be the best time to buy a new property as rates are now becoming more affordable.

2023 saw a huge hike in mortgage rates, largely due to the Bank of England increasing the base interest rate to 5.25%.

According to Zoopla, fixed mortgage rates peaked at 6.44% which was a stark contrast to the historic lows.

But will mortgage rates continue to rise in 2024 or will they begin to drop?

The good news is that mortgage rates are already starting to come down. News reports in early January 2024 suggest that mortgage lenders are already cutting rates.

One of the biggest UK lenders, Halifax, has cut their mortgage interest rates by close to one percentage point and mortgage brokers are expecting other lenders to now follow suit.

It is important to note however that not all mortgage products will be reduced, so it’s wise to speak to a mortgage broker to understand which ones have now become more affordable for you.

How mortgage rates are dropping at the start of 2024

Towards the end of 2023, you’d be lucky to get a mortgage rate below 5%. Since January 2024, 5 year fixed rate deals are now being offered at below 4%. However, this rate is only available currently for a remortgage with a 60% loan-to-value.

Media outlets are reporting that a 2 year fixed deal should soon fall below 4.5%.

As we continue to move through the year, Benwell Daykin expect these below 5% rates will move to other mortgage products too, as well as other lenders.

When rates decrease, buyers tend to have better affordability. This means they can look to make offers on properties which they previously may not have been able to afford.

As such, we expect house prices to remain at their current levels, if not increase slightly.

Houses should begin to sell faster too, as increased affordability means more people will be looking to purchase property.

Key things to remember as mortgage rates drop

Remember to always speak to a mortgage broker before making a decision on which mortgage product to go for. Benwell Daykin offers free initial mortgage advice which can help you to decide which product is best for you based on your own circumstances.

Fixed rates are a great way to lock in lower interest rates but be aware these rates could go down further. If you lock in for a long period of time then you will be missing out on these further drops. Of course, rates could rise too which would obviously act in your favour!

Remember also to look out for fees. Some lenders offer lower rates but include a fee when signing up for the mortgage.

After COVID-19 and following the sharp inflation rate rise, many were expecting house prices to crash.

The reality is that house prices did indeed dip, but not by a huge amount. According to Nationwide, prices have dropped just 2% in 2023.

What’s more, other reports have suggested that although there is an overall drop for the year, prices are actually on the up since the Autumn.

So why haven’t prices dropped significantly? The team at Benwell Daykin list some of their thoughts.

Interest rates have remained stable

When the Bank of England began to raise interest rates, many took a step back from looking to move due to affordability. If interest rates rise then mortgage costs do too. This meant that many home owners had to reduce their prices to continue to entice buyers.

Now however, interest rates have remained at a steady 5.25 per cent since August 2023.

House prices have already dipped to reflect this change and have remained stable along with the rate of interest.

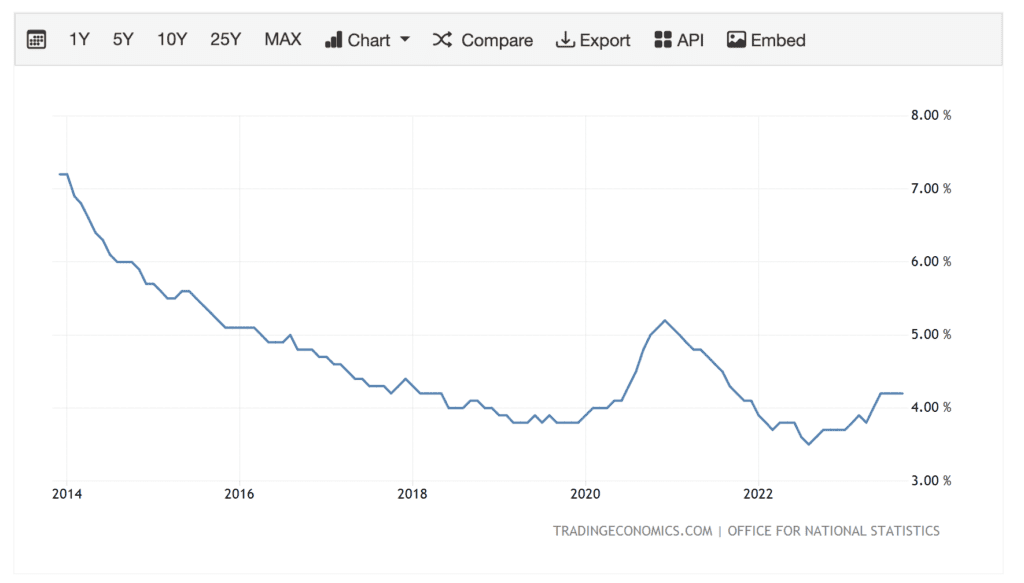

Unemployment remains steady

When the population struggles to find work then this, of course, has a knock on effect on the economy.

Unemployment has risen in 2023, however it is much lower than both 2014 and 2021 according to Trading Economics.

Mortgage rates are coming down

When interest rates began to rise, so did mortgage rates. Some home owner’s monthly payments began to triple.

Some others had made offers on higher priced houses but suddenly couldn’t afford them when rates went up.

As such, home owners again lowered prices to combat this.

Now mortgage rates are dropping once again. Although they are certainly nowhere near where they were a couple of years ago, some lenders now have products at below 5 per cent.

If rates fall further, this could actually boost house prices.

This puts confidence back in the property market and heightens affordability once again.

Inflation has slowed

Inflation cooled more than expected in October 2023, from 6.7 per cent to 4.6 per cent.

It has now more than halved from its peak of 11.1 per cent in October 2022. This has been a relief for many who are struggling with the cost of living.

Inflation slowing is another confidence boost to the property market.

So will we see a market crash?

Unfortunately, we don’t have a crystal ball here at Benwell Daykin.

All the above seems very positive and if things continue as they have been doing, we would expect to see house prices increase rather than decrease.

However, the world and the economy is ever changing and we just don’t know what tomorrow might bring.

How much is your house worth right now? Where ever you are in Nottinghamshire, contact our friendly team to find out today.

Today Nationwide have stated that property prices are on the rise once again.

Prices had dipped marginally in most areas of the country and many experts predicted there would be a further decline throughout the remainder of the year. Thankfully, this now appears not to be the case.

What about Nottingham property?

Nottingham has always remained one of the strongest area for housing price growth across the country. This year is no exception.

Despite decreases in almost every area of the UK, Nottingham hasn’t really been hit. Prices remain strong and growth has actually continued!

If we look at Hometrack’s data, Nottingham sits top of every major UK city for growth in the last 12 months. This stands currently at +2.9%. Sitting at second place is Birmingham at +2.7% and Sheffield with +2.3%. If we compare this to London, they saw a decline in the last year with -0.5%.

Looking short term, Nottingham prices increase in the last 3 months by 0.3%.

Why did property prices decrease in other areas?

Property prices have decreased slightly in 2023 mainly due to the rise in interest rates. This meant that more people were cautious when it came to applying for mortgages. As a result, less people were then looking for houses which brought prices down.

It is important to note however that it is only a small decline. Prices dropped across the board by just -1.1% in 2023. (Hometrack)

What is the average property price now?

The average home increased in price from £257,808 in September to £259,423 in October, according to Nationwide‘s latest house price index. This index is based on their own mortgage data but is very accurate as they are one of the largest UK lenders.

In Nottingham, the average property price is now £202,400.

Why have house prices generally increased?

Data suggests that many buyers have been holding off buying due to the rise in mortgage interest rates. Now it appears that they cannot wait any longer and have decided to purchase, regardless.

Other contributing factors include strong employment and a short supply of available properties.

What does this mean for home owners?

For those waiting to sell, you’d be forgiven if you were putting this off after listening to the national news.

Whilst we would advise anyone to remain cautious with the constant changing interest rates, now is definitely not a bad time to place your property on the market.

With the increase in buyer confidence now across the board we should see more people looking at every property and battling to make the highest offer.

How much is my property worth?

We can offer you a free, no obligation property valuation. Simply call us on 0115 990 2007 or use the form below.

October 2023 and the Nottingham lettings market is booming.

According to the BBC, landlords are now seeing at least 25 interested parties looking at every individual property.

Looking back at the rental market in 2019, this was down to an average of just 6 parties looking at the same house or flat.

Rental price rises

This news now comes at the time when the average rental price outside of London has hit £1,278 – a new record. This alone is a 10 per cent increase since July.

Looking specifically at Nottingham, the average rental price for those letting their property is £1502 pcm (Homes.co.uk)

Why are rents rising in Nottingham?

Rents are rising in Nottingham for a number of reasons. The city has an extremely large student population and many students are now returning after COVID.

Many individuals, couples and families are also now turning to the rental market since high mortgage rates have made home ownership a distant prospect.

Another reason for such a large amount of applications for each property is that supply is fairly low.

Many landlords are looking to sell due to mortgage rates, tax changes, EPC changes and more. This means that there is a much smaller range of properties for prospective tenants to choose from.

What does this mean for landlords?

If you’re looking at letting a property to tenants then your void periods are likely to be minimal. This should obviously save you some money, especially for those who still have a buy to let mortgage.

If you were considering selling your property then it may be an idea to wait and let it out instead.

How can tenants successfully rent their dream property?

With demand so high, letting agent Benwell Daykin can offer a few tips on how to successfully rent a property.

Start looking early to ensure you aren’t left without a home. With 25 parties looking at each rental property, the chances of getting rejected are unfortunately high

Ensure you have all your paperwork in place, including ID, payslips and references

Calculate your finances and make sure you aren’t out pricing yourself. Remember to include funds for your deposit, bills, furniture and more

Set up alerts on Rightmove or Zoopla. This means you will get an email as soon as new lettings properties are listed

Want more lettings information?

Talk to Benwell Daykin who can help both landlords and tenants. Call 0115 990 2007 today. We can even provide free valuations.

We have been successfully matching tenants to rental properties for years and offer free advice over the phone.

You may have heard recently that there’s been another change to gas boiler policies in the UK.

Until recently, the UK was to phase out gas boilers in new build homes by 2025 and ban them completely from new homes by 2033.

This, however, has now been extended to 2035.

What was the original gas boiler ban plan?

The UK government has been asking homeowners to switch their traditional gas boilers to heat pumps as a more environmentally friendly option. Originally they were offering a grant of £5,000 although this has now been increased to £6,500.

The uptake for this has apparently been fairly slow which could be a reason for the change in deadline.

What is a heat pump?

In the shortest possible terms, a heat pump transfers captured heat from the air outside to the inside of a property. This is then used to fuel the property’s central or underfloor heating and in some cases also provide hot running water.

How does a heat pump benefit home owners?

Heat pumps are renowned for their energy efficiency, resulting in significant savings on heating costs compared to traditional gas boiler systems. They achieve high energy efficiency ratios, leading to lower utility bills and reduced carbon emissions. Essentially, although heat pumps can have a large initial outlay, there are savings to be had.

Landlords could also benefit from heat pumps as another way to entice tenants to rent their homes. During the current cost of living crisis, any reduction in household bills for tenants can be seen as a positive thing.

If you’re considering applying for a grant, you can do so on the government website.

What will these new announcements mean for home owners?

Firstly, if you were considering making your home more energy efficient then you now save even more money with a larger grant. You can apply for this via the government website.

Secondly, if your boiler needs to be replaced imminently then you should still have the choice as to go for a lower cost traditional system or a more expensive eat pump. This could be a big plus if you’re feeling the pinch with rising mortgage costs.

Thirdly, if you’re looking to sell your home in the near future, this could be an attractive selling point. We would advise though to do your calculations to ensure the profits made on selling your home outweigh the cost of a heat pump. Benwell Daykin can help with advising you how much your property is worth. Just call 0115 990 2007 to get a free property valuation.

If you’re wondering what option to choose, contact Benwell Daykin in Ruddington who will be able to offer some advice based on your situation.

This year the Uk economy has hit some challenges. Energy costs, high inflation, plus much more. With this, house prices have changed and so have mortgage payments.

The latest figures from Nationwide state that house prices have fallen at their fastest rate in August since 2009. Although this sounds like doom and gloom, the average house price back then was £162,112 compared to today’s prices of £286,000. This means that anyone looking to move should still turn a tidy profit.

Although this probably isn’t new news to anyone,mortgage payments have now increased in line with rising interest rates. For some families, this has seen monthly repayments triple.

So with mortgage payments rising, is it now cheaper to buy or to rent?

The answer, according to property site Zoopla, is it depends where you live!

Currently, those who live in London and the south are likely to now find it cheaper to rent a property.

The average UK rent is £1,163 per month, while average mortgage repayments are £1,285 for first-time buyers with a 15% deposit.

In Ruddington and Nottinghamshire, you are still likely to be financially better off when buying a property instead. The difference though is tiny, with just £56 between the average rental payment and the average mortgage payment.

So why is this?

Put simply, house prices have been much higher in the south for a long time. Historically low mortgage rates meant that buyers could afford larger houses and pay less. Now they’re paying more.

If you are struggling with mortgage payments, please talk to Benwell Daykin who will be able to offer free, impartial financial advice from our fully regulated advisor. We would also be happy to provide a free property valuation to see how much your property is now worth.

Call 0115 990 2007 and talk to our friendly team today.

On Thursday 3rd August 2023, the Bank of England raised interest rates by another quarter of a percent. This has now taken the base rate to 5.25 per cent and is the 14th consecutive hike. This is also the highest interest rate since March 2008, the year of the financial crisis.

So what does this mean for you?

Why are interest rate rises happening?

By rising interest rates, the Bank of England is hoping to bring down inflation. Inflation is very high right now which is contributing to our cost of living crisis. By increasing interest rates, the BoE are hoping that many will stop spending and save money instead. This, in turn, should hopefully lower the price of goods.

What will happen to mortgage payments?

The interest rate increase can be a troubling time for some. For instance, there are over 1.4 million people in the UK who are on a variable rate residential mortgage. This means that their payments fluctuate along with interest rates.

Some home owners could now see hundreds of pounds added to their monthly payments which, during a cost of living crisis, is definitely not ideal.

What can you do to ease any pressure?

There are several things you can do to ease pressure if your mortgage bills are rising. The first is talk to a qualified mortgage broker. Whilst this blog can offer guidance, every financial situation is different. You can talk to a qualified broker for free by calling our offices on 0115 990 2007.

You can also talk to your lender. Some are now offering a switch to interest-only products. This means you only pay the interest on your mortgage every month, rather than the full payment. Whilst this does lower your monthly costs, be aware that you won’t be making payments towards your home, only to the lender’s fees. This will likely extend the term of your mortgage.

Moving to a fixed-rate mortgage could also help. If you are on a variable rate where your payments fluctuate, you may be financially better off by fixing in the rate for 2, 5 or 10 years. Again, talk to a qualified mortgage broker to see which option is best for you.

The good news

It’s not all doom and gloom, however. Santander, for example, actually cut their mortgage rates ahead of the base rate rise. So there are deals still to be had if you talk to a qualified mortgage broker.

It may also be easier for you to purchase a property right now. House prices have dipped slightly which means you may be able to afford that property of your dreams.

In an astonishing twist of events, the UK housing market has defied all expectations by experiencing an unforeseen surge in house prices during June 2023. This unexpected upward trajectory has left homeowners, potential buyers, and industry experts astounded.

The surprise monthly rise of 0.1% reversed a 0.1% fall in May and confounded economist forecasts of a 0.3% fall. It pushed the average cost of a house in the UK up slightly to £262,239. This is according to Nationwide.

Two-year fixed-rate mortgage rates have continued to climb past 6% after the Bank of England increased interest rates by half a point to 5% in June in an attempt to curb stubbornly high inflation. The average two-year fixed deal edged higher again on Friday, to 6.39% from 6.37% the day before, according to Moneyfacts. The average five-year fix rose to 5.96% from 5.94%.

Nottingham growth tops UK

Nottingham property price growth still continues to outperform all areas in the UK according to Hometrack.

In the last 12 months, property prices rose in the area by 10.9%. This means a £150,000 property grew to £165,000 in just 1 year.

In the last 3 months alone, Nottingham property prices grew by 1.4%.

The average Nottingham house price now stands at £198,000.

It’s always a good time to sell

Ready to see how much you have made on your property since purchasing?

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.